Saying no quickly to uninteresting ideas is valuable in investing – there is a massive universe of stocks to track and spending time on the wrong ones is a recipe for disaster. While people regularly discuss how they selected their portfolio, they don’t often discuss why they rejected different stocks. Some investors have a fixed criteria or checklist to filter out ideas, but usually the best ideas are nuanced and failing financial screens can be an edge (some market participants have already filtered the idea out). The filtering process requires rational but intense scrutiny and a high bar so that only the best ideas sift through. We want to iterate over many ideas quickly without missing the best ones; too many false negatives (ideas you think are bad but are actually good) and the opportunity cost stacks up. A few passes I made recently and why:

Gates Industrial Corp (GTES) –

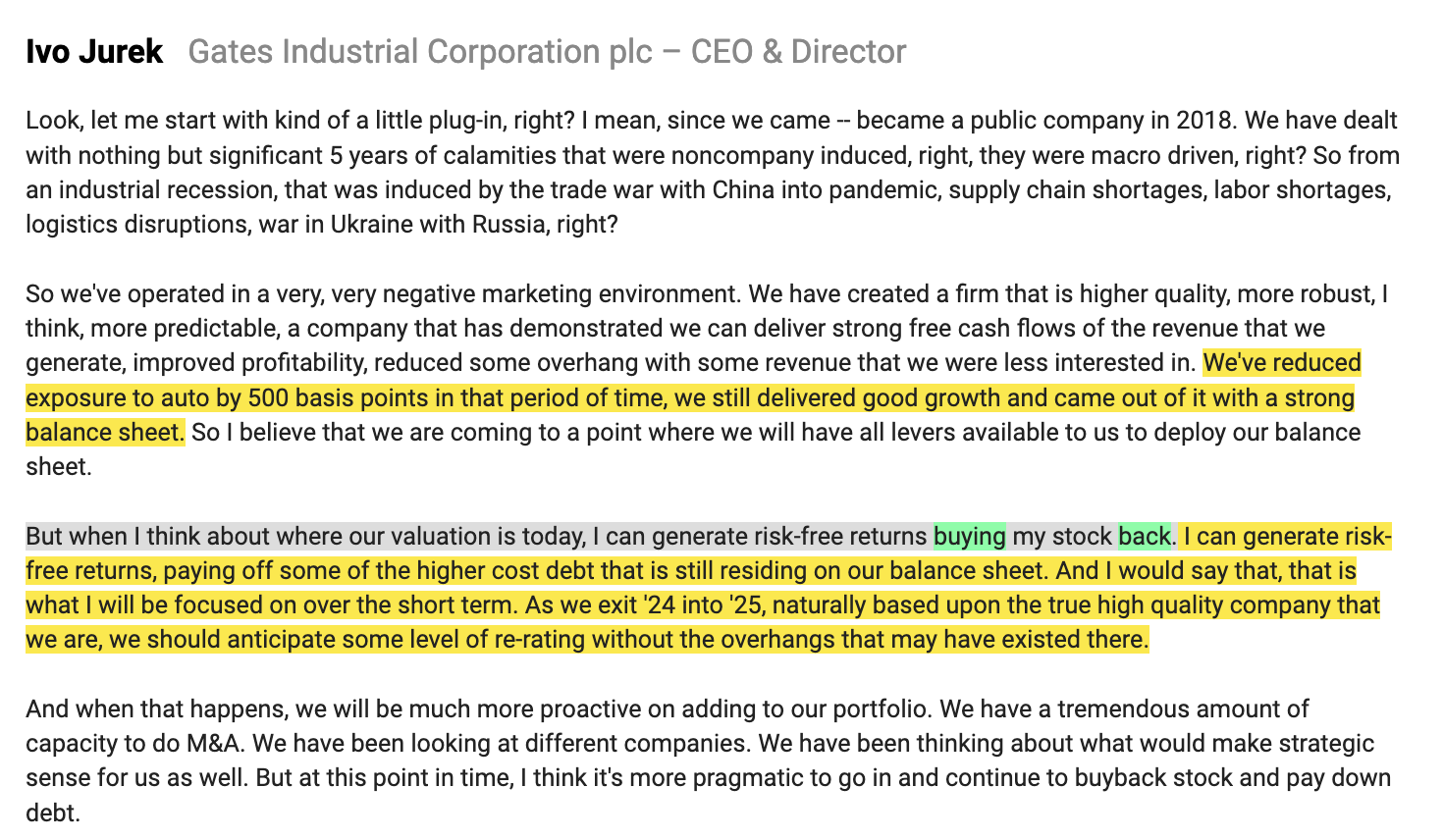

What caught my eye about the company was the CEO’s devoted stance on buybacks. The stock trades at 8-9x P/E whereas comps trade at 12-13x P/E. This is an industrial company with a long history selling power transmission products, and bulls argue there’s a secular industry tailwind (EVs + data centers). The stock is probably cheap, but I don’t really see a good “angle” – there’s no reason why I have real edge here and there’s no optionality i.e. room for explosive upside. There are other ideas I’d rather own with a similar setup, namely AER – excellent management and capital allocation, trades below book value (which is probably significantly understated), will continue compounding capital at MDD growth rate in a strong industry upcycle that I have confidence in. Why not just buy more AER (I find the “why not buy more X” question super useful in making quick passes)?

Lifecore has a critical CDMO asset that investors believe will be bought by another party soon. Stock price is at $7-8 but CDMO asset could fetch $15-25+ in a sale. Two CDMO assets were recently acquired for huge premiums and there’s a logical buyer for the Lifecore asset (LLY). Absent a sale, Lifecore probably doesn’t generate enough cash to stay afloat and goes bankrupt. As a rule of thumb, I prefer binary situations where I’m okay with owning the underlying business in the negative outcome (no sale) – this isn’t a strict filter though because given a large enough margin of safety to the conservatively calculated expected value of the situation, the stock may still be worth owning.

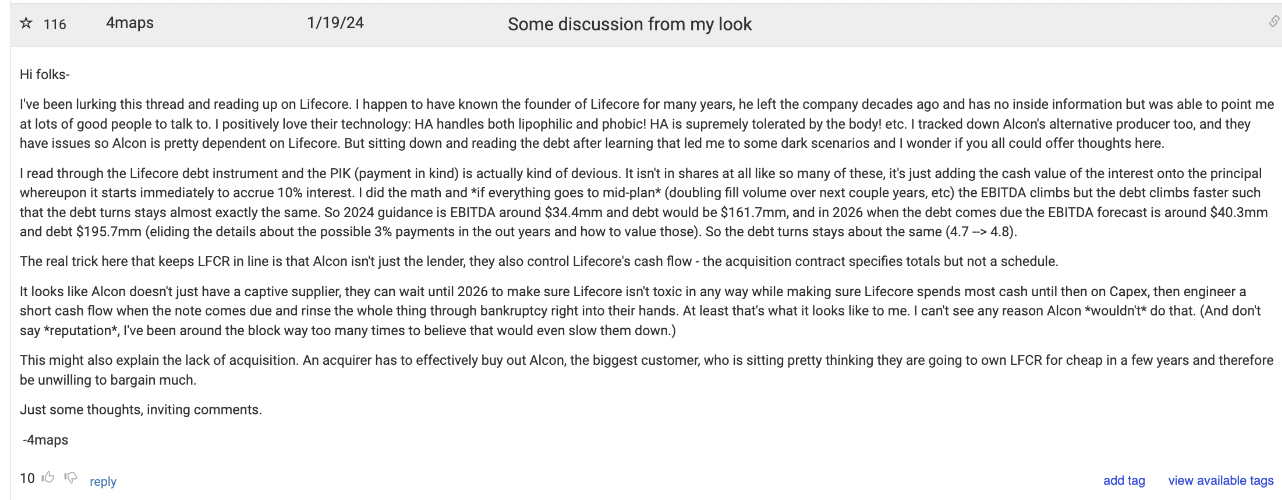

Teetering with the idea of doing a deeper dive because I couldn’t find a compelling reason not to, I came across this comment on the LFCR VIC post:

Basically, Alcon, a customer and creditor of LFCR, can control Lifecore’s cash flow by virtue of their supply agreement and holds a predatory PIK agreement – together these make it near impossible for Lifecore to de-lever. From Alcon’s perspective, they can sit and wait for a LFCR bankruptcy and own the asset in a few years. From an acquirer’s perspective, they need to buy out Alcon – Alcon would be unwilling to bargain much given their position, which prevents a major hurdle to sale.

Given incentives are aligned for a “no-sale” outcome + LFCR bankruptcy, I’m not really interested in playing.

Cardno (CDD.AX) –

Australian company in liquidation mode, has significant receivables to recover from various customers. Fintwit makes it seem like a 20-30% upside outcome (by end of H1 ’24) is close to guaranteed.

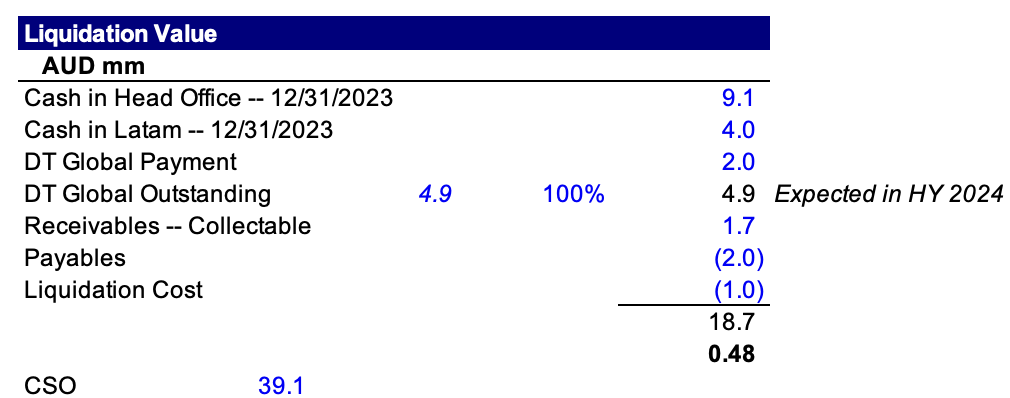

I agree on 20% upside in a scenario (0.48 vs 0.40 price today) where receivables from a core customer, DT Global, are fully recovered. If these receivables are not recovered, there’s 12.5% downside risk (to 0.35). This means the market is pricing in ~40% odds of recovery which seems reasonable to me. I don’t have a strong variant view on collection odds so this is a pass.