Two seventy bio (NASDAQ: TSVT) is a $262mm market cap cash-burning biotech spin-off operating in the competitive CAR-T space. Bluebird bio spun out its oncology assets as two seventy bio in early 2021 – Bluebird CEO Nick Leschly left to lead two seventy and pioneer the first CAR-T therapy for multiple myeloma (MM).

Instead, over the next two years, Leschly evaporated billions in investor capital, plowing cash into unproductive R&D. TSVT stock price rightfully fell from above $20 down below $2 as concern grew that Leschly would drive the company into bankruptcy. Yet against this backdrop, the story for two seventy’s standout asset (the “GoodCo”), Abecma, continued to improve.

In 2013, Bluebird entered a master services agreement with Bristol-Myers Squib concerning oncology R&D. In 2016, Bristol-Myers Squib saw promising developments from Idecabtagene vicleucel (ide-cel aka Abecma), and exercised their option to license the drug. BMS and Bluebird amended this agreement from a licensing arrangement to profit share – Bluebird and BMS would split revenue and costs for Abecma 50-50. Bluebird also gave up ex-US rights on Abecma for an upfront payment of $200mm from BMS (after reading further, you may see that this was a mistake).

Bluebird and BMS embarked on the KarMMa clinical trials to show ide-cel’s efficacy and soon after the spin-out of Abecma into two seventy, Abecma received FDA approval for the 4L+ setting (four prior lines of treatment) in multiple myeloma. There are ~30k new multiple myeloma cases per year in the US and ~4k among these move into the 4L+ setting. Ide-cel costs around $450k/patient – accounting for the fact that not all 4L+ patients are fit to receive a CAR-T therapy, this is a $500mm-$1bn addressable market.

Bluebird and BMS continued with the KarMMa-3 study, aiming to expand Abecma into the 3L+ setting and quadruple the addressable market from ~4k to ~16k patients in the US. Meanwhile, Janssen Pharmaceuticals (Johnson & Johnson) and Legend Biotech co-developed cilta-cel (aka CARVYKTI), another CAR-T therapy for MM, and received 4L+ approval. Janssen and Legend initiated the Cartitude-4 trial in hopes of expanding cilta-cel to the 3L+ setting. At 16k patients, it’s not unreasonable to believe this is a $8-10bn market opportunity that will be split between first-movers ide-cel and cilta-cel.

While ide-cel and cilta-cel took large strides penetrating the 4L+ market, generating hundreds of millions in revenue in 2022 and 2023, and preparing for further expansion in earlier-line settings, Nick Leschly seemed distracted… rather than focus on two seventy’s crown jewel, Abecma, he was intent on dreaming up new R&D projects. Two seventy was losing nearly $300mm in cash per year because of Leschly’s recklessness, frustrating investors and leading to TSVT being valued at $100-200mm while Abecma could arguably be worth billions.

In late 2023, Engine Capital sent a letter to two seventy’s board imploring them to sever ties with Leschly among other steps to maximize shareholder value. The activists were successful – Leschly left, Chip Baird, former Bluebird CFO, was appointed CEO, and an expansive cost cutting program was put in place. Two seventy laid of 40% of its workforce and suggested a plan 350mm in cumulative cost savings through 2025.

At this point, one would think the market would recognize Abecma’s true value and two seventy would begin trading towards it. But the company’s struggles continued…

Q3 ’23 and Q4 ’23 were rough for Abecma, showing large yoy revenue declines. While BMS explained Q3 declines were a result of manufacturing issues, Q4 was simply attributed to “competitive pressures”. The consensus opinion among investors rightfully seems to be that cilta-cel is a better therapy on balance than ide-cel. Cartitude-4 paints a clear, strong picture for cilta-cel: overall response rate is high and there is a sustained progression free survival benefit (PFS; exactly what it sounds like – amount of time a patient can live without the cancer worsening). KarMMa-3 shows lower absolute response rates, but a strong PFS benefit relative to the standard of care arm, though there isn’t a “plateau” of sustained benefit in the PFS curve. These studies are very difficult to compare, especially because KarMMa-3 is a crossover trial (more on this later…). Investors may have thought that the overwhelming demand for CAR-T therapies would outpace manufacturing capacity and lentiviral vector supply (key raw material for the CAR-T therapy; was also used in COVID-vaccines which created a shortage for sometime that was still normalizing), thus physicians would just use whichever therapy they have access to (and thus the “better” one doesn’t really matter). But the Q4 comment on competitive pressure from two seventy probably solidifies that cilta-cel has a step-up on them in the market.

Note that while Abecma is doing hundreds of millions in annualized revenue, the net profit to TSVT remains low (utilization of manufacturing facilities is a big element here – there seems to be a lot of operating leverage) and were the company to remain exclusively in the 4L+ setting, it would struggle to generate sizable cash flow, especially if cilta-cel were to move to 3L+.

So now we move to current day – Abecma and cilta-cel are both vying for 3L+ approval. Investors thought that this approval would be straightforward, but the FDA took a harsher than expected stance on early deaths in the Cartitude and KarMMa trials. BMS/TSVT and Janssen/Legend argued that these early deaths were a result of improper bridging therapy protocol, not ide-cel or cilta-cel itself. The FDA holds advisory committee meetings (ODAC – Oncologic Drugs Advisory Committee) before making a final decision on approval. Cilta-cel cleared ODAC with a unanimous 11-0 vote. For BMS/TSVT, things were a little bit more complicated…

KarMMa-3 was a crossover trial. There were two arms – the ide-cel arm and the standard of care arm. However, patients were allowed to crossover from the ide-cel arm into the standard of care arm if they showed significant disease progression. This is a patient-centric design because it allows patients to get access to the best possible therapy, but complicates interpretation of the overall survival (OS) endpoint. The panel generally seemed to agree that OS was the same or slightly better with ide-cel. But the crux of the debate came down to the following: is the risk of early deaths acceptable in the context of additional clinical benefit from moving ide-cel to the 3L+ setting? BMS argued early deaths were due to the bridging therapy routine prior to ide-cel treatment – bridging therapy was restricted to one cycle and couldn’t really be individualized as it is in the real world. Some of the ODAC members explained that as bridging therapy improves and CAR-T is used more in real-world settings, the risk of early deaths should subside. On the benefit side, there was significant discordance regarding the PFS benefit offered by ide-cel – while median PFS improves with ide-cel, some ODAC members seemed to disagree on the sustenance of the PFS benefit – the PFS curves eventually come back together implying that PFS benefit subsides after ~1 year. But this interpretation is arguably also confounded by the crossover nature of the trial. Seeing a lower potential clinical benefit vs. the same risks discussed for cilta-cel, the panel was split and voted 8-3 in favor of Abecma.

While 90% of FDA decisions align with ODAC, it’s worth investigating the 3 votes against Abecma to finetune our probability that FDA dissents with ODAC in this case. One reviewer, Dan Spratt, believed there was no confounding due to crossover on the OS curve, and that there was no real clinical benefit to Abecma. To be honest, I didn’t completely understand his reasoning and I think the rest of the ODAC panel pushed it aside as well. The Chair, Ravi Madan, also voted no – his reasoning seemed to revolve around there being minimal clinical benefit vs. the early deaths risk. Given that other ODAC members with more experience in multiple myeloma like Dr. Kwok mention that 1-year PFS uplift is sufficient in real-world treatment settings and the FDA never really contested Abecma’s PFS benefit, I’m comfortable believing the FDA will side with Abecma if they approach the question the same way the panel did. I’m not too sure about the third NO vote – Dr. Vasan wasn’t as vocal in the discussion. I may be over-analyzing, but I did also sense some confliction within the panel members that voted YES – it didn’t seem like a clear-cut, easy decision for them though this could also be a function of the chair’s strong vocal negative bias.

The FDA came into ODAC with two key issues: 1) early deaths and 2) risk-benefit. The panel took a unanimous stance on early deaths likely being due to bridging therapy across cilta-cel and ide-cel. Risk benefit was clear for cilta-cel but less clear for ide-cel, though the myeloma experts on the panel and the FDA both expressed a view that Abecma does have a strong PFS benefit.

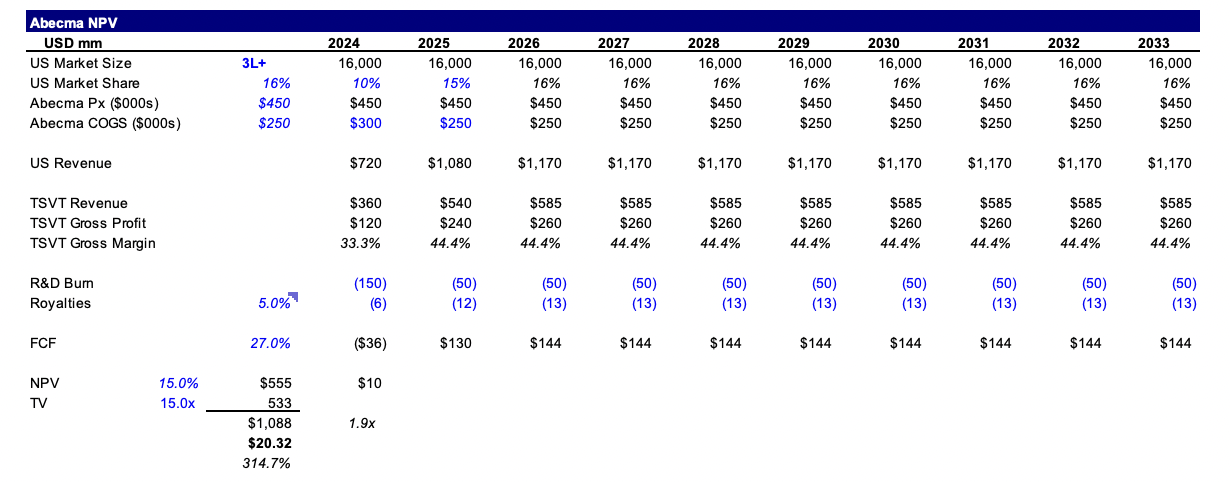

Why spend so much time discussing ODAC? The FDA should have a final decision on Abecma’s sBLA as soon as April 5th (this is cilta-cel’s decision date so some speculate the FDA may approve both together). TSVT currently trades at $5. I think Abecma is worth $15-30. I’ll discuss valuation soon, but I think the market may have angst about sBLA approval given TSVT’s value-destructive history and be failing to recognize that there’s a pretty high probability (90+%) that Abecma gets 3L+ approval. Buying post-catalyst may be less lucrative if TSVT gaps up.

Some quick math:

I’m effectively valuing TSVT at 2x peak revenue of ~$600mm (i.e. $1.2bn peak revenue for Abecma in the US). This implies 16% market penetration which I think is conservative even with competitive pressures from cilta-cel. Cilta-cel has an aggressive guide to $5bn+ peak revenues in an $8-10bn market. That still leaves $3-5bn for ide-cel. One could argue other gene therapies gain FDA approval and commercial success before ide-cel hits peak revenue, and that’s a fair point, but I think the market is likely to value TSVT in the above manner if TSVT garners traction in the 3L+ setting.

If Abecma does realize greater market penetration, the numbers get crazy and there’s no reason TSVT can’t trade up to $50.

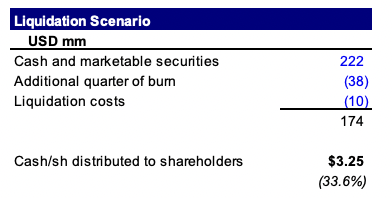

If ABECMA doesn’t get ODAC approval, I would hope Chip makes the right decision (maybe with some pressure from Engine or other institutional shareholders) to return capital to shareholders. In a liquidation scenario, shareholders get $3-4 of cash back. Tactically, buying at a $4 handle is a lot more effective than $5 or $6 because of the greater % downside protection.

When he joined two seventy, Nick Leschly was technically not CEO – he titled himself Chief Kairos Officer. Kairos is an old Greek word that refers to the timeliness of an action. Nick discusses Kairos in the context of cancer – timely CAR-T therapy adds quality years to a patient’s life. I’d argue that now, the opportunity in TSVT perfectly reflects Kairos – this is the perfect time for action and to be buying. I’ve struggled in the past with having conviction in my theses and sizing positions up to a point where they generate meaningful returns. Ironically, I may need to take a page from Nick’s playbook and embody Kairos buy taking advantage of the incredible opportunity in front of me.