Nagarro (DB:NA9; €1.2bn TEV) is a global IT services company domiciled in Germany. They spun off from Allgeier in late 2021. The company trades at a large discount to American peers, despite impressive growth over the past decade (though from a much smaller base and reliance on inorganic levers).

NTM estimates from Koyfin, Rev CAGR from Bonsai Partners Letter

The prudent investor is probably wary of theses that begin with “invest in the lowest-valued name in the sector” – there is usually a good justification for the market serving up a company at a hefty discount to peers. For Nagarro, there are surface level red flags that may trigger an instinctive “flight” reaction in investors and lead to a quick pass:

-

Nagarro has an unusual corporate structure – in place of a CFO, there is a “Finance Council”. Traditional CXO Roles are replaced by Global Business Unit (GBU) leaders. There is no global headquarters – the company operates in a remote, decentralized manner.

-

The CEO and co-founder of Nagarro, Manas Fuloria, changed his name to Manas Human. A commentor on VIC wrote: “Nagarro is run by a guy who changed his last name to “Human” Seems like another sketchy German co.”

-

Until recently, Nagarro had an unknown auditor that many investors were unfamiliar with, Lohr and Company GmbH. Combined with lackluster free cash flow conversion and significant capital allocation towards M&A, one might believe there is plenty of room to subtly “cook the books”. From Twitter: “M&A of subsidiaries can be problematic. CEO control reminds of EBIX. Don’t like roll-ups hence ‘next’”

An intuitive short seller target, one would expect the problems leading to a low valuation to be thoroughly exposed by an intelligent short. WirtschaftsWoche published a short report – their “smoking gun”: many of the phone numbers listed on Nagarro’s website did not work (nobody picked up the phone and there was no way to leave a message!). An investor on a German forum commented: “Wirecard 2.0.”

Unable to find a reasonable explanation for why Nagarro deserves to be so cheap, I dove deeper. What I found is that the “red flags” lay the foundation for a compelling bull case. Nagarro’s eccentric approach is driving stellar results like a 67 net promoter score in Q3 ’23. Management is genuine and incentives are aligned – Manas owns 0.6% of the company, they are returning capital to shareholders via buybacks, and focused on further cash conversion.

Manas responded to comment in the short report, taking thesis points as constructive criticism rather than an attack. Management heard concerns about their auditor and switched to KPMG. They listened to concerns about their use of factoring (selling invoices upfront to generate near-term cash) and ended this practice.

This is a company that does things differently but cares about its shareholders, is constantly working to improve, and producing results. The past few years have been difficult for IT services companies as customers cut non-essential programs and wage inflation hit margins – Nagarro was forced to lay off a significant portion of its workforce. But as macro headwinds dissipate, Nagarro should begin to return to its strong pre-COVID growth profile and margins should expand. Management is guiding for ~20% yoy medium-term organic growth and 18% adjusted EBITDA margins by 2026. I believe these targets are conservative-to-reasonable for a 30+% pre-COVID grower with peers that have hit >18% adj. EBITDA margins. Nevertheless, I use even more conservative numbers in my valuation below.

I think Nagarro is worth €190 vs. ~€76 stock price today, or a ~30% IRR over the next 8 years.

The numbers are clear, and the crux of our investment case rests on disavowing the red flags investors are quick to label Nagarro with.

Let’s start with Manas. Aside from writing poetry books, lobbying for action against climate change, and riding his bike on the crowded roads of Gurugram, Manas loves to tweet! Oh and of course, Manas is the CEO of a multinational IT services company. Manas seems distracted and unfocused on growing Nagarro, yet the company showed organic growth of >20% CAGR from 2018-2022! Yes, this is less than peers, but it is nothing to scoff at and gives credence to forward guidance.

Manas is an eccentric personality, and this spills over into Nagarro: the decentralized nature of the company and cultural quirks (like annual retreats and investor days where speakers can talk about anything they please – including poetry) are evidence. But why punish eccentricity when it works? If Tesla prices in a leadership premium, why shouldn’t Nagarro?

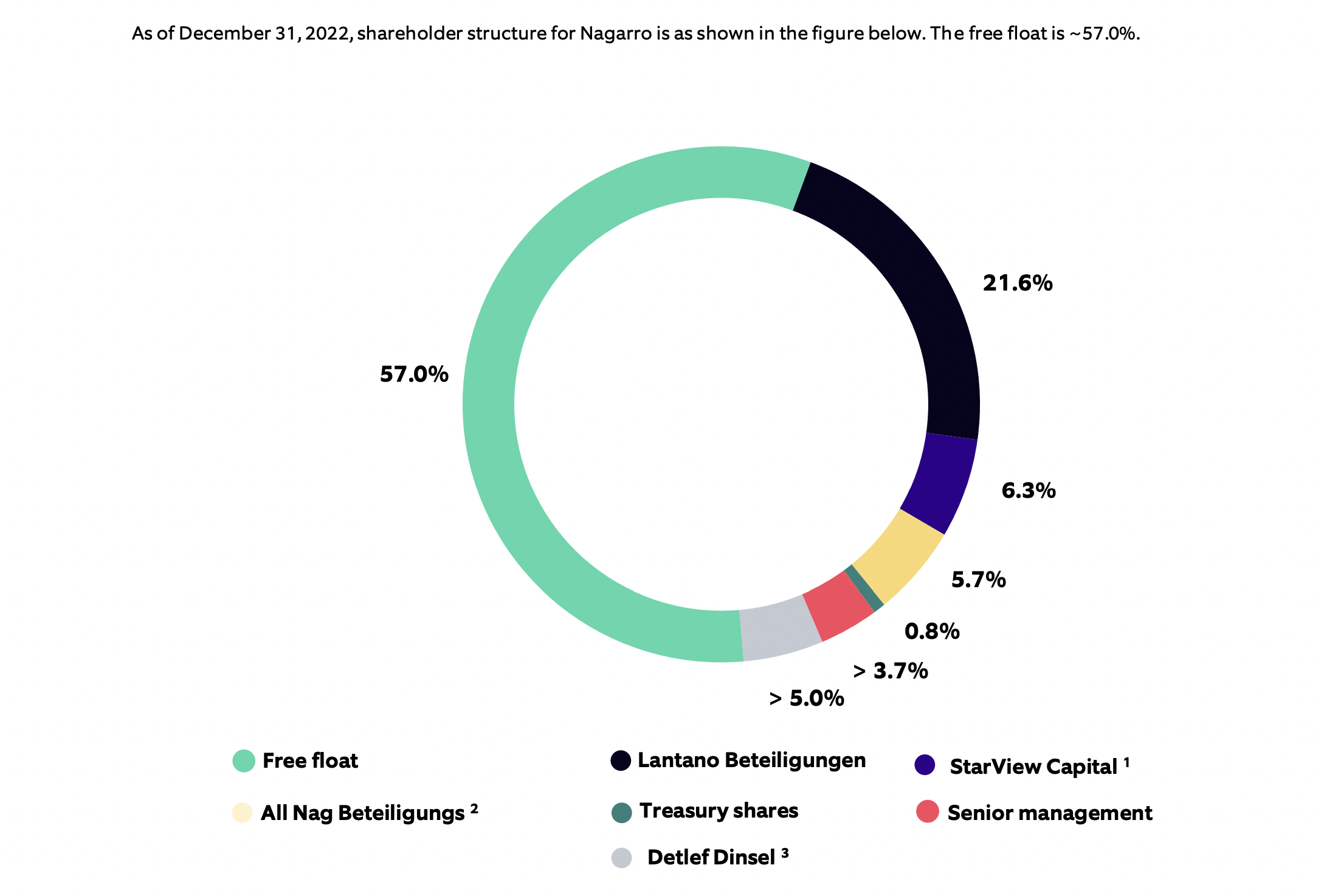

And what about the rest of the management team and other insiders? Over 40% of shares are owned by insiders, primarily Vikram Seghal (StarView Management), co-founder and “COO” (custodian of operational excellence), Detlef Dinsel, vice board chair, and Carl Georg Duerschmidt (Lantano Beteilligungen), board chair.

Insiders bought at much higher prices than where the stock trades at today and are heavily incentivized to inspire stock price appreciation.

When asked about why the stock is cheap (over email, Oct. 2022), management said they were unsure, but had a few thoughts:

-

Germany listing

-

Weak cash conversion due to growth

-

Uneasiness with auditing firm

-

Uneasiness with Nagarro work structure (decentralized nature of business, no HQ)

Since the email, two of these concerns, cash conversion and auditor, have been resolved. The Germany listing is a barrier to entry for some funds but on its own, not a compelling justification for why Nagarro is cheap.

Nagarro’s decentralized structure is worth discussing further. In a recent Tegus transcript, the interviewer grills a former Finance Director at Nagarro about how Nagarro’s financials are compiled and reviewed given the lack of a CFO. Neeraj Chibba, the de-facto “leader” of the Finance Council has an engineering background, not a financial one. Nagarro’s business units each operate independently, and their financials must be compiled from the bottom-up – given the lack of a CFO and a small auditor with ~30 employees, it’s believable that an investor may doubt the accuracy of Nagarro’s financials – the Tegus interviewer seemed to. This is an extreme source of angst in my opinion – if you believe Nagarro is a quality company and management is not attempting to scam you, it feels unlikely their accounting is falsified. Given their auditor change and cash flow conversion starting to show through, “accuracy of accounting” concerns should be put to rest.

A more pressing problem with Nagarro’s decentralized approach was that certain centralized controls are necessary for a company to operate properly. Significant time was invested in implementing centralized project management and talent distribution processes so that different Global Business Units (GBUs) could access company-wide resources fairly. These seem like relatively easy problems to resolve though, especially given the advantages a GBU structure offers – each vertical Nagarro operates in (finance, healthcare, tech, etc.) has its own GBU. The GBU sources projects independently and can take a tailored approach to sales. Horizontal resources are offered across GBUs – for example, experts in AI, ERP, cloud migration, etc. In Manas’s words (or Jensen Huang’s), Nagarro is architected for its employees to operate in an optimal fashion.

With a little bit of research and maybe a couple of calls with Manas, it’s not hard to see why Nagarro’s eccentric approach is a neutral-to-positive factor. Yet maybe some investors end up passing on Nagarro due to its mismanaged investor relations.

Nagarro’s listed IR “expert” is Gagan Bakshi – yet Gagan is a managing director at Nagarro and by no means an IR specialist. In fact, he barely speaks English… I don’t mean to dump on Gagan but he is not the right person to articulate the long case for Nagarro and enthuse investors.

Really, the right person to talk to is Manas – but even though Manas is highly accessible as far as CEOs go, he has said that he has been stretched thin by investor calls and will be offloading more of that responsibility to Gagan.

On top of all the idiosyncratic reasons why Nagarro is cheap, the IT services industry has been in a downcycle since late 2022 – new modernization projects slowed as recession realities settled in for customers. Many major players have missed guidance or revised downwards, including Nagarro. While some investors use downward revisions and misses as evidence of Nagarro being a low-quality, mismanaged company, Nagarro has continued to grow MSD year-over-year while comps report negative top-line growth.

Nagarro charges lower prices than more recognizable brands like EPAM or Globant, but executes with similar levels of success (evidenced by high NPS and low attrition rates). A significant contributor to Nagarro’s success is their use of offshore hubs – Nagarro is a highly regarded employer in India. Endava recently paid 3x sales to acquire a small offshore presence in India, citing outsourcing as a critical long-term trend – Nagarro trades at a fraction of this multiple and is best positioned to take advantage of continued offshoring.

The market has further interpreted recent advances in generative AI as a headwind for IT services providers. The first order effect of AI is efficiency gains for software teams, resulting in less work that needs to be outsourced to EPAM, Nagarro, etc. “Easier” projects related to testing or customer support likely become less defensible in the age of AI. But Nagarro prides itself on taking on complex, hairy challenges for its customers and “thinking breakthroughs” – as large enterprise customers begin to think about how to incorporate generative AI in their workflows, Nagarro will be best poised to help. I think that it’s likely generative AI ends up a net tailwind for Nagarro.

While investors fight over which of the 25-30x P/E EPAM, Globant, or Endava present the best opportunity in an IT services downcycle, Nagarro is the odd one out: it sits at an unjustifiably cheap valuation. Investors craft surface-level narratives to discredit Nagarro’s progress and justify a quick pass, but a deeper dive shows the full picture: a high-quality company lead by excellent, well-aligned management, poised to compound share price at >30% for the next decade.